NO SUSTAINABLE INVESTMENT OBJECTIVE

This financial product promotes environmental or social characteristics, but does not have as its objective sustainable investment.

ENVIRONMENT OR SOCIAL CHARACTERISTICS OF THE FINANCIAL PRODUCT

When determining what investments to make for the Sub-Fund, as part of the Delegated Investment Managers’ Sustainable Investment Policy, the Delegated Investment Manager considers environmental and social factors (at industry or company specific level), in the assessment of the strength of individual businesses and the risks associated with them. In respect of the environmental factors the Delegated Investment Manager takes into consideration, these include for example, assessing through its own due diligence and external third-party data, a company’s policies towards managing emissions, energy usage and waste management. In respect of the social factors the Delegated Investment Manager takes into consideration, these include for example focus that a company has on talent management and retention of employees and policies surrounding health, and safety and working practices.

In addition to the foregoing part of the investment process for the Sub-Fund, the Delegated Investment Manager also applies active exclusionary screening in the investment process to reduce Sustainability Risks. As part of the process the Delegated Investment Manager excludes from investment in the Sub-Fund companies that fall within certain listed categories (set out in further detail below).

As part of the Delegated Investment Manager’s Sustainable Investment Policy and investment process, the Delegated Investment Manager takes principal adverse impacts (”PAI”) on sustainability factors into account in its investment decision making process.

A reference benchmark has not been designated for the purpose of attaining the environmental or social characteristics promoted by the financial product.

INVESTMENT STRATEGY

The Delegated Investment Manager’s Sustainable Investment Policy consists of a multistage approach to integrating ESG factors and Sustainability Risks in investment decisions. The Delegated Investment Manager focuses on governance factors. The particular focus relates to two key elements of the Delegated Investment Manager’s investment philosophy, namely:

- investing in businesses where the shareholders’ interests are aligned with the company’s management; and

- where the company’s management has a track record of good capital allocation decisions, which have created long term value for all shareholders.

When determining what investments to make for the Sub-Fund, as part of the Delegated Investment Managers’ Sustainable Investment Policy, the Delegated Investment Manager considers environmental and social factors (at industry or company specific level), in the assessment of the strength of individual businesses and the risks associated with them. In respect of the environmental factors the Delegated Investment Manager takes into consideration, these include for example, assessing through its own due diligence and external third-party data, a company’s policies towards managing emissions, energy usage and waste management. In respect of the social factors the Delegated Investment Manager takes into consideration, these include for example a focus that a company has on talent management and retention of employees and policies surrounding health, and safety and working practices.

The Delegated Investment Manager uses a number of resources to deepen its knowledge of business and governance practices at investee companies. To supplement its own due diligence efforts, the Delegated Investment Manager utilises resources, such as proxy voting services, external sustainability research and engagement groups through the UN PRI and/or Climate Action 100+. Internal due diligence includes writing to management teams to source additional information. The Delegated Investment Manager’s due diligence of a company’s ESG policies will place the company into the context of global best-practice and assess the potential materiality of the risk associated with these policies to the company’s earnings.

The Delegated Investment Manager believes that dialogue with investee companies as well as proxy voting are ways to add value to the investment process and that stronger ESG practices will be reflected in better company and stock performance. Through constructive engagement with company management, from a medium term to long-term perspective, the Delegated Investment Manager seeks to help promote an investee company’s sustainable growth. Additionally, the Delegated Investment Manager seeks to enhance ESG practices at investee companies through proxy voting. The Delegated Investment Manager views this direct engagement with investee companies as an essential part of the investment process.

The Delegated Investment Manager applies its own proprietary systems and research, aiming to develop an accurate understanding and assessment of a portfolio company’s ESG practices. While the Delegated Investment Manager uses Refinitiv’s Asset4 and MSCI ESG external research data as its principal providers for ESG metrics, the Delegated Investment Manager also conducts its own proprietary research to arrive at independent ratings. This proprietary analysis aims to supplement the gaps in data, to address some the material pitfalls of vendor data, notably placing greater overall emphasis on corporate governance and remove exclusive reliance on a third-party vendor. In addition, where gaps exist in company disclosures, the Delegated Investment Manager actively engages with the company to improve transparency.

Based on the Delegated Investment Manager’s qualitative assessment of a company’s practices within the context of global best practices, disclosures and goal setting, and any third-party data that is available, on completion of the review, the Delegated Investment Manager assigns a rating of ”A”, ”B”, ”C” or ”D”, (i) ”A” being high quality practices, (ii) ”B” being moderate quality practices, (iii) ”C” being low quality practices; or (iv) ”D” whereby a review by the Delegated Investment Manager’s analyst team will be requested. Where a ”D” rating is assigned to a company, the company will be excluded by the Delegated Investment Manager from investment in the Sub-Fund. Within the overall assessment the Delegated Investment Manager also indicates a qualitative assessment of the company’s risk as it relates to Sustainability Risks, accounting, litigation any other relevant risk that may potentially impair earnings. The Delegated Investment Manager will also indicate if there is an opportunity for the analysts to engage with the company.

In addition to the foregoing part of the investment process for the Sub-Fund, the Delegated Investment Manager also applies exclusionary screening. As part of the process the Delegated Investment Manager excludes from investment in the Sub-Fund companies that fall within any of the following categories: (i) are involved in the production or trade in weapons and munitions*[1], (ii) are involved in the production of tobacco*, (iii) are involved in gambling, casinos and equivalent enterprises*, (iv) are involved in the production of thermal coal, (v) are involved in the production of oil from oil sands, (vi) are involved in adult entertainment enterprises; and (vii) are rated ”D” by the Chief Sustainability Officer.

[1] *This does not apply to project sponsors who are not substantially involved in these activities. “Not substantially involved” means that the activity concerned is ancillary to a project sponsor’s primary operations and comprises less than 5% of total annual revenue.

As a signatory to the Climate Action 100+ initiative the Delegated Investment Manager is committed to collectively engaging companies to (i) curb emissions, (ii) improve governance; and (iii) strengthen climate-related financial disclosures. The Delegated Investment Manager believes that improving company governance, curbing emissions and strengthening disclosures increases the risk-adjusted return potential, whilst also serving to help tackle the systemic risk that climate change represents.

In connection with adhering to the UN PRI, the Delegated Investment Manager is committed to the following six principles (the ”UN PRI Principles”):

- to incorporate ESG issues into investment analysis and decision-making processes;

- to be an active owner and to incorporate ESG factors into its ownership policies and practices;

- to seek appropriate disclosure on ESG factors by the entities in which it invests in;

- to promote acceptance and implementation of the UN PRI Principles within the investment industry;

- to work with the PRI Secretariat and other signatories to enhance their effectiveness in implementing the UN PRI Principles; and

- to report on our activities and progress towards implementing the UN PRI Principles.

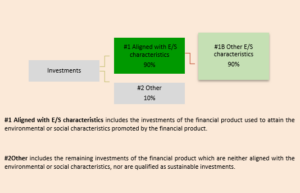

PROPORTION OF INVESTMENTS

The Sub-Fund aims to hold a minimum of 90% of investments of the Sub-Fund’s portfolio that are aligned with the environmental or social characteristics promoted by the Sub-Fund. The Sub-Fund does not commit to holding sustainable investments. The Sub-Fund will not hold more than 10% of investments that are not aligned with the environmental or social characteristics promoted by the Sub-Fund and are not sustainable investments, and which fall into the “Other” section of the Sub-Fund (further details of which are set out below).

Please note that while the Sub-Fund aims to achieve the asset allocation targets outlined above, these figures may fluctuate during the investment period and ultimately, as with any investment target, may not be attained. The exact asset allocation of the Sub-Fund will be reported in the Sub-Fund’s periodic report for the relevant reference period.

MONITORING OF ENVIRONMENTAL OR SOCIAL CHARACTERISTICS

The Delegated Investment Manager will assess and track the performance of companies with regards to environmental and/or social characteristics promoted by the Sub-Fund using a number of the sustainability indicators as detailed below, including companies that (i) hold ISO 14001 (or equivalent) and/or ISO 50001 (or equivalent) certifications, (ii) are members of the UN Global Compact and have adopted UN Sustainable Development Goals in their long-term planning, (iii) are aligned with the Paris Agreement and those that are EU Taxonomy aligned, (iv) hold OHAS 18001/45001 (or equivalent), ISO 27001 (IT security), and/or ISO 9001 (quality management) certifications; and (v) have publicly documented human rights policies, ethics and corruption policies and sufficient whistleblower protections in place (as further detailed below). The sustainability indicators will be used to measure the attainment of the environmental and social characteristics promoted by the Sub-Fund.

METHODOLOGIES OF ENVIRONMENTAL OR SOCIAL CHARACTERISTICS

As part of the investment process, the Delegated Investment Manager considers a variety of indicators to measure the environmental and/or social characteristics promoted by the Sub-Fund. The Delegated Investment Manager monitors energy management, emissions and waste management by identifying the companies that hold ISO 14001 (or equivalent) and/or ISO 50001 (or equivalent) certifications. The Delegated Investment Manager tracks how many companies are members of the UN Global Compact and have adopted UN Sustainable Development Goals in their long-term planning. The Delegated Investment Manager also monitors the number of companies that have aligned with the Paris Agreement and those that are EU Taxonomy aligned. Finally, where data is available (and relevant), the Delegated Investment Manager will assess long-term Scope 1, 2 and 3 emissions performance.

For the purposes of assessing social characteristics, the Delegated Investment Manager identifies those companies that hold OHAS 18001/45001 (or equivalent) (occupational health and safety management), ISO 27001 (IT security), and/or ISO 9001 (quality management) certifications. The Delegated Investment Manager also identifies those companies that have publicly documented human rights policies, ethics and corruption policies and sufficient whistleblower protections in place.

DATA SOURCES AND PROCESSING

The Delegated Investment Manager uses a range of data providers when assessing a portfolio company’s ESG practices, in addition to its own proprietary analysis and research. The primary third party data providers are Refinitiv and MSCI, in addition to Bloomberg.

As noted above, in addition to utilising third party data providers, the Delegated Investment Manager also conducts its own proprietary research to arrive at independent ratings. This proprietary analysis aims to supplement the gaps in data, to address some the material pitfalls of vendor data, notably placing greater overall emphasis on corporate governance and remove exclusive reliance on a third-party vendor. Where gaps exist in company disclosures, the Delegated Investment Manager actively engages with the company to improve transparency.

The Delegated Investment Manager will also utilise third-party data, namely Refinitiv and Bloomberg, when considering PAI on sustainability factors in its investment decision making process.

LIMITATIONS TO METHODOLOGIES AND DATA

While data sets across Asian markets are currently limited, the Delegated Investment Manager’s expectation is that data coverage will continue to expand over time as more markets introduce climate related reporting regimes to comply with the Paris Agreement. Third party vendors provide high quality research, however the Delegated Investment Manager recognises the limitations in external ESG methodologies and does not rely on it exclusively. The Delegated Investment Manager is satisfied such limitations do not affect how the environmental or social characteristics promoted by the Sub-Fund are met due to the processes it has implemented to mitigate such limitations as the Delegated Investment Manager has developed its own proprietary ESG investment process and the Delegated Investment Manager will assess third party vendors research as part of its ongoing due diligence.

DUE DILIGENCE

In respect of due diligence, as part of the Delegated Investment Managers’ Sustainable Investment Policy, as outlined above, when determining the environmental factors the Delegated Investment Manager takes into consideration, these include for example, assessing through its own due diligence and external third-party data, a company’s policies towards managing emissions, energy usage and waste management.

Furthermore, as outlined above, the Delegated Investment Manager uses a number of resources to deepen its knowledge of business and governance practices at investee companies. To supplement its own due diligence efforts, the Delegated Investment Manager utilises resources, such as proxy voting services, external sustainability research and engagement groups through the UN PRI and/or Climate Action 100+. Internal due diligence includes writing to management teams to source additional information. The Delegated Investment Manager’s due diligence of a company’s ESG policies will place the company into the context of global best-practice and assess the potential materiality of the risk associated with these policies to the company’s earnings.

ENGAGEMENT POLICIES

The Delegated Investment Manger views engagement with investee companies as an essential part of the investment process. Where the Sub-Fund has invested in a company and the Delegated Investment Manager has developed a relationship with the management team of that company, the Delegated Investment Manager will engage with companies seeking to promote positive change on ESG matters.

The Delegated Investment Manager believes that dialogue with investee companies as well as proxy voting are ways to add value to the investment process and that stronger ESG practices will be reflected in better company and stock performance. Through constructive engagement with company management, from a medium term to long-term perspective, the Delegated Investment Manager seeks to help promote an investee company’s sustainable growth. Additionally, the Delegated Investment Manager seeks to enhance ESG practices at investee companies through proxy voting.

DESIGNATED REFERENCE BENCHMARK

A reference benchmark has not been designated for the purpose of attaining the environmental or social characteristics promoted by the financial product.

PRINCIPAL ADVERSE IMPACTS STATEMENT

Since the adoption of Article 8 status of the Fund, the delegated investment manager has been considering the Principal Adverse Impact (“PAI”) framework set out within the Regulatory Technical Standards (“RTS”) applicable under the EU Sustainable Finance Disclosure Regulation (SFDR). In 2023, the manager completed an extensive exercise to develop the systems and data tools to ensure it was sufficiently equipped to provide reporting around the mandatory PAI indicators and two additional voluntary indicators as required. The delegated investment manager has leveraged data sets available through its primary data provider Refinitiv and utilizes additional data from Bloomberg. For complete information on the data sets used and the methodology of our RTS process please refer to the delegated investment manager’s sustainability policy. The delegated investment manager will report the PAI indicators as part of its ongoing quarterly reporting package and will utilize data as an additional engagement tool when providing constructive engagement to company management and boards. In addition, where relevant it will use the data to inform voting around environmental issues.

REMUNERATION POLICY

ALIGNMENT OF INTEREST

There is a high degree of alignment of interests between employees and clients at Dalton which is achieved through high levels of employee equity ownership and remuneration linked to client outcomes. Indeed, a high level of alignment between employees and clients is a cultural aspect of the organization itself.

EQUITY OWNERSHIP

Dalton is entirely employee-owned, with no intention of changing this structure. The majority owner and CIO views it as essential that senior members of the investment team are themselves “owner-operators”, much like the companies Dalton invests in. Equity in Dalton is gradually being sold by 3 of Dalton’s 4 founding partners to the next generation (CIO retaining majority). Employees are invited to participate in these purchases as a recognition of their performance and importance to the future of Dalton. Recommendations on which employees to invite are made by the Management Committee and signed-off by Dalton’s majority owner annually. As of June 2023, 13 employees have become new partners of the firm (17 partners total when you include the 4 founders).

REMUNERATION

Recommendations on compensation for Dalton team members are proposed by the Management Committee and ultimately signed off by the majority shareholder and CIO.

Dalton’s primary driver of profitability is providing clients with attractive risk-adjusted returns and superior client servicing and retention. In this manner, Dalton believes that discretionary bonuses help to align the interest of employees and clients.

At Dalton, fixed salaries are kept at a moderate level (Dalton uses an external compensation benchmarking service to ensure fairness), while bonus payments reflect an individual’s contribution to the business over the long-term.

While evaluating the Analyst Team, the Management Committee takes into account an analyst’s research efforts and contribution to overall firm profitability. Bonus are based upon 1) the profitability of Dalton, 2) performance of the investment funds they are managing, and 3) contribution to the overall firm. Team members are assessed on various hard metrics, such as absolute and relative returns over 1-year and 5-year periods, as well as soft metrics (team collaboration/communication, engagement activities, marketing contribution, commitment to ESG and adherence to the investment philosophy).

Dalton expects its investment team to reinvest 50% of their bonus into Dalton’s funds with an objective of having 3 to 5 times their annual salaries aligned with clients through their fund investments.

Long-term successful employees can buy into or further increase their share in Dalton. Dalton believes this system aligns investment team members with its clients and locks them into the firm for the long term.

CO-INVESTMENT

Considering Dalton’s expectation on bonus reinvestment, the investment team members have the majority of their net worth invested in Dalton’s portfolio stocks. As at end-June 2023, Dalton team members had $64m invested in Dalton funds.